What AI’s Next Act Might Look Like

Last Updated: July 08, 2026

LPL’s Midyear Outlook 2026 has arrived. While much of the report provides the types of content you might expect from LPL Research, such as forecasts for GDP, earnings, and interest rates, this edition of the publication is unique in its focus on four key themes that we believe will shape capital markets performance in the second half. Here we focus on one of those themes: AI’s Next Act.

Evolving AI Narrative

AI is likely to remain a key driver of equity markets during the second half of 2026, but the narrative is evolving. The market is shifting from enthusiasm over AI infrastructure spending and rapid earnings growth toward a more balanced debate about returns on investment and which companies will ultimately benefit most.

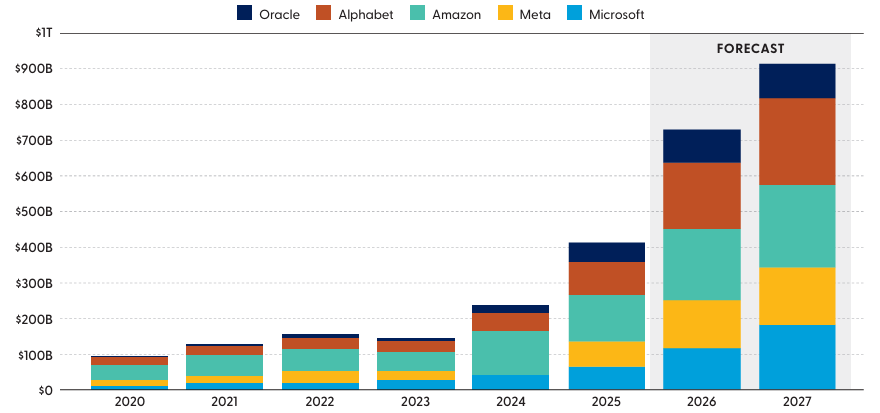

Still, the scale of AI investment remains extraordinary. Alphabet (GOOG/L), Amazon (AMZN), Meta (META), Microsoft (MSFT), and Oracle (ORCL) are collectively on track to spend more than $750 billion on AI infrastructure in 2026, with spending potentially exceeding $1 trillion in 2027. This buildout has fueled exceptional earnings growth, particularly in technology and semiconductors. At the same time, AI adoption remains relatively early, suggesting significant productivity benefits may still lie ahead as usage broadens across industries.

Hyperscaler Capital Expenditures Continue to Rise

Source: LPL Research, Bloomberg 06/30/26

Disclosure: Oracle’s fiscal year ends May 31. All other companies report on a calendar year basis. Estimates may not materialize as predicted and are subject to change.

Despite investor concerns that the AI investment cycle could be nearing a peak, several factors suggest the buildout may have further runway. Major AI leaders continue to signal higher spending plans, and constraints related to data center capacity, power availability, specialized components, and regulation could extend the investment cycle.

The Shift to Monetization

Markets are becoming increasingly focused on the returns of these investments. Equity valuations and analysts’ forecasts already reflect expectations for margin expansion and productivity gains. As a result, investors are likely to demand greater evidence that AI is translating into higher revenue, lower costs, and stronger profits. While some spending may prove inefficient, the broader opportunity remains substantial if companies can successfully monetize AI capabilities.

The coming earnings seasons may provide more insight into this transition, particularly as companies outside the technology sector increasingly disclose how AI is improving operations and profitability.

Beyond Technology

As AI adoption broadens, the benefits may extend well beyond the technology sector. Industrials could emerge as notable beneficiaries, using AI to enhance logistics, manufacturing efficiency, and supply chain management, potentially supporting margin expansion. At the same time, some software companies could face disruption as AI capabilities become more widely embedded across business applications.

Bottom Line

AI is entering a new phase. The market is moving from pricing in promise to pricing in execution. Rather than signaling the end of the AI theme, this transition may create a more selective environment in which companies that demonstrate successful monetization are rewarded, while those that fail to deliver face greater valuation pressure and volatility. Recent volatility in semiconductor stocks suggests this transition is underway. Investors should focus less on who is spending the most and more on who is generating measurable returns from those investments.

Find more on AI’s next act in LPL Research's Midyear Outlook 2026: Policy, Buildouts, and Bottlenecks.