The Tension Between Market Optimism and Policy Reality

Last Updated: June 24, 2026

Today's blog is written by Chris Fasciano, chief market strategist at Commonwealth. He represents Commonwealth in various media appearances, advisor speaking events, and Commonwealth conferences. He also oversees and mentors a dynamic team of investment research analysts who specialize in equity and fixed income markets. Prior to this role, Chris spent 10 years as one of the firm’s portfolio managers, involved with asset allocation and fund selection. With a deep background in small- and mid-cap stock research, Chris is uniquely positioned to analyze the latest economic data and offer valuable insights on navigating today’s volatile markets. Chris Fasciano is a guest writer and is not affiliated with LPL Financial.

Following last weekend’s announcement of a deal between the U.S. and Iran to bring the war in the Middle East to an end, markets rallied and oil prices dropped. This reaction is logical given that elevated oil prices have contributed to accelerating inflation data. However, the Federal Reserve’s (Fed) June meeting reinforced that inflation remains a primary concern for policy makers.

This dynamic highlights the competing forces that currently shape markets. On one hand, easing geopolitical risk and falling oil prices support optimism. On the other hand, persistent inflation keeps pressure on the Fed to potentially tighten monetary policy. These crosscurrents are likely to play a significant role in stock and bond performance over the remainder of the year.

The Positives of the Memorandum of Understanding

Investor focus has centered on the Memorandum of Understanding (MOU) between the U.S. and Iran, which provides a 60-day window to negotiate a final agreement. Initial discussions are already underway.

Markets quickly moved past what had been a major concern: that sustained higher oil prices would continue to drive inflation higher. That risk had stood in contrast to an otherwise supportive backdrop of strong corporate earnings and a stabilizing labor market.

At the center of the market’s reaction is the Strait of Hormuz. From an investor perspective, its reopening is the most consequential part of the agreement. If the Strait returns to full capacity within 30 days, oil prices are unlikely to remain a meaningful source of upward inflation pressure.

So far, markets appear confident. Oil prices have declined to levels not seen since early in the conflict, suggesting investors are already pricing in a normalization of supply.

West Texas Oil Prices Discounting a Return to Normal

Source: LPL Research, Bloomberg Year to date through June 22, 2026

Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results. Estimates may not develop as predicted and are subject to change.

The “West Texas Oil Prices Discounting a Return to Normal” chart illustrates that market participants have a high degree of confidence that oil prices are headed lower over the remainder of the year. As of now, futures prices indicate oil will move below $70 per barrel in early 2027. This implies a broad expectation that recent supply disruptions will prove temporary rather than structural.

While this is encouraging for the inflation outlook, it does little to address the Fed’s near-term challenge.

The Federal Reserve’s Focus on the Present

The June Fed meeting — Chairman Kevin Warsh’s first — made it clear that policymakers remain firmly focused on inflation. Warsh reiterated the Fed’s commitment to its 2% inflation target and signaled little willingness to adjust policy based on recent declines in oil prices alone. Markets interpreted this as a hawkish shift.

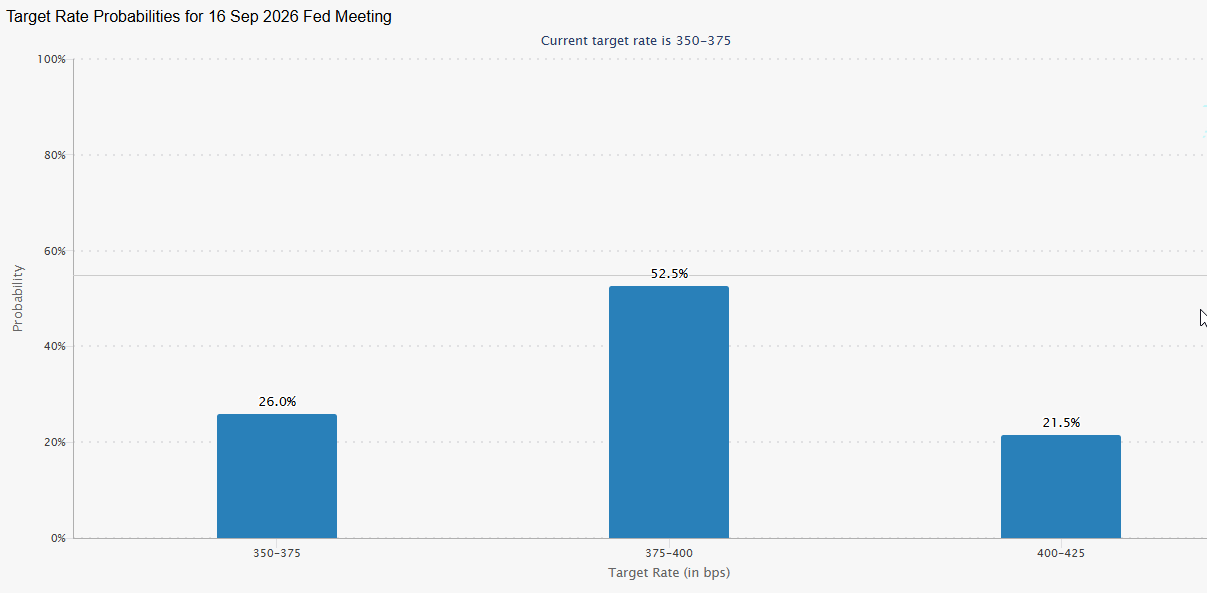

Rates Poised to Rise

Source: LPL Research, CME Fedwatch 06-22-26

Disclosure: Past performance is no guarantee of future results.

The “Rates Poised to Rise” chart shows that most market participants now believe that short-term interest rates will be higher by the end of the Fed’s September meeting.

But that was not the only thing that investors were left to think about after last week’s meeting. Chairman Warsh announced the formation of five tasks forces to look at various Fed policies and operations. These task forces will look at communication, balance sheet, reliance on existing data sources, productivity and jobs, and inflation frameworks.

Warsh has long believed that reform is necessary at the Fed and he clearly aims to deliver. The biggest impact from potential reforms for markets is that it appears a Warsh Fed will provide the market with less forward guidance. Warsh went as far as to say he could offer no guidance on what the Fed’s next move would be. While markets will adapt, reduced guidance could lead to increased volatility, particularly in interest rate-sensitive areas.

Those changes will take time to play out. In the meantime, investors need to navigate the positive sentiment of lower oil prices with what the Fed might do.

The Path Forward Most Likely Lies Somewhere in Between

If the Strait is open to full capacity within 30 days, then oil prices will remain low, prices for gas at the pump should trend downwards and ultimately supply chains will return to normal. It will certainly take time for consumer and producer prices to move back to their February levels but the momentum to do so should be in place.

If there is evidence that this is happening, then perhaps the Fed would be willing to look through short-term data when it comes to potentially raising interest rates. In that case, Wednesday’s reaction to Chairman Warsh’s first press conference would prove to be overly negative through the rearview mirror.

Earnings Continue to Hold the Key

Equity markets have rallied strongly from the March lows, with the S&P 500 gaining nearly 18%. Given ongoing uncertainty around geopolitics and Fed policy, near-term volatility would not be surprising.

Attention will soon turn to second-quarter earnings, where expectations are high. Analysts are projecting approximately 22% year-over-year growth for the S&P 500. While this raises the risk of disappointment, recent history suggests resilience. Over the past five quarters, companies have continued to deliver strong results despite policy and trade-related uncertainties. If earnings momentum continues, it should provide a foundation for markets over the longer term — even if volatility persists in the short term.

Also, despite all the excitement about the Space X (SPCX) initial public offering and the upcoming deals for Anthropic and Open AI, this has been a year for diversification across equity markets. The Russell 1000 large cap value index has outperformed its growth counterpart by 1,300 basis points. The small cap Russell 2000 also performed better than the S&P 500 by over 1,000 basis points. Finally, international stocks have continued to outperform U.S. stocks after a strong 2025.

Markets are navigating a balancing act: optimism around falling oil prices and easing geopolitical risk is colliding with a Federal Reserve still focused on inflation. History shows diversification remains the best way to navigate uncertainty about the future and yet still participate in any market upside due to strong earnings growth. And this year has been a reminder of exactly that.

Asset allocation does not ensure a profit or protect against a loss.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.