Using the Late 90s as a Comp, the AI Boom Still Has Legs

Jeff Buchbinder | Chief Equity Strategist

Last Updated: May 12, 2026

Many have drawn the comparison between the current AI buildout with the dotcom period in the late 1990s, when the infrastructure for the internet was built. It’s a sensible comparison to make because of the massive amount of capital deployed to commercialize the buildout of revolutionary and life-changing technology. It’s also a reasonable comparison to make because technology stocks drove one of the biggest stock market rallies in history more than 25 years ago, and some are using similar language today when discussing the potential (and we underscore potential) of AI and bidding up the valuations of AI companies poised to benefit.

Pros and Cons of the 1990s Comparison

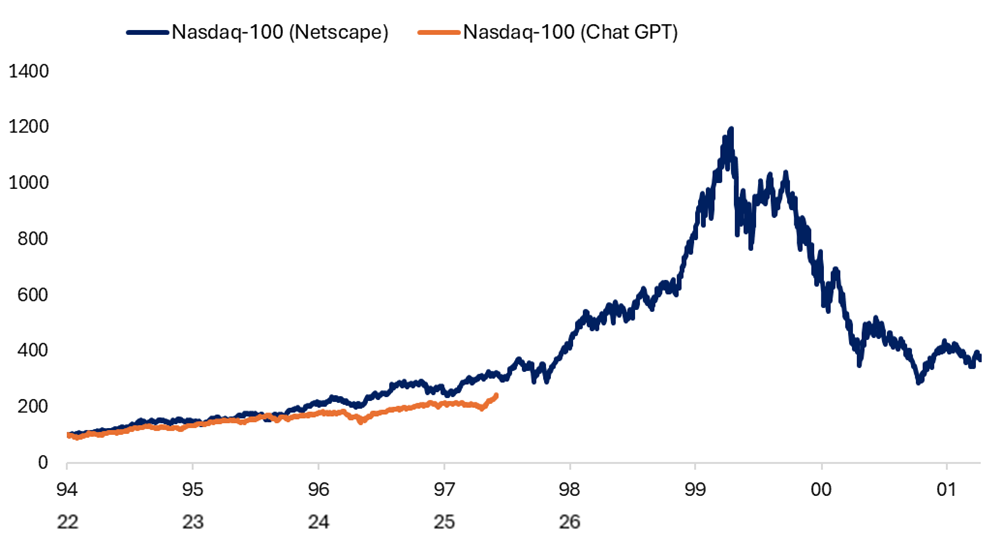

While we don’t think this is a great comparison for a number of reasons — which we cover below — it is interesting to line up the path of the tech-heavy Nasdaq-100 Index from the start of the AI era, which we mark at the launch of ChatGPT, to the birth of the modern internet, i.e., the launch of the first browser, Netscape (later acquired by AOL). As illustrated in the “Based on the Dotcom Era Comparison, the AI Bull Market Seems Fairly Reserved” chart, the Nasdaq-100 advance in recent years is more gradual than that of the advance over a similar four-year time frame. Based on this comparison, the current bull market — nearly four years old — still may have plenty of life left in it. The Nasdaq-100 is up more than 140% since ChatGPT was launched, while the index gained over 1090% from when Netscape was first released until the peak of the dotcom bubble in March 2000.

We’re not saying history will repeat and that the Nasdaq 100 will be up another 900% before crashing. We are simply making the point that the current stock market trajectory is more rational than you might think, and this may be more like 1997 than late 1999 or early 2000.

Based on the Dotcom Era Comparison, the AI Bull Market Seems Fairly Reserved

Source: LPL Research, FactSet 05/11/26 (Data series normalized to 100 on 12/15/94 and 11/30/22)

Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Reasons This Time is Different

We admit these are dangerous words in investing. But when comparing historical periods, every time is different. Despite the similarities between dotcom and AI from a financial market perspective, there are more differences. Some of them include:

Stronger leadership. The leaders are funding the AI buildout mostly with internal cash flow and not speculative capital raising. Their business models are much more diversified than the website-oriented business models of the dotcom era, and their balance sheets are much stronger than the fiber optic equipment makers of the late 1990s. Some AI sub-segments may be showing some dotcom-like behavior, but that’s not where public market leadership is.

Grounded valuations. In March 2000, the technology sector peaked at a valuation of 58 times consensus forward earnings, compared to 25 today. During the dotcom era, eyeballs and clicks were oft-cited valuation measures. Today is about earnings, revenue, and cash flows.

More rational IPOs. The technology IPOs are much larger today, with proven business models and sizable revenue streams. Even for companies operating at a loss today, it’s much easier to see a path to profitability.

AI is early in its cycle. Today, the buildout is centered around AI infrastructure, while the AI adoption phase has barely begun. During dotcom, the frothy period of the cycle featured consumer websites that could never be sufficiently monetized even after the infrastructure was in place. Today, we don’t know who the AI adoption winners will be. The strong balance sheets of the infrastructure builders are a good start, paving the way for many AI adoption winners to materialize in the future.

Summary

There are clear similarities between the AI bull market cycle and the dotcom boom of the late 1990s. Technology stocks provided stock market leadership; valuations were elevated; there were segments of market speculation; and technology advances were life changing. But in terms of what companies are leading the current technology revolution, how the stock market is valuing them, how much speculation is taking place, and what stage of the cycle we’re in, we see important distinctions.

Bottom line, we think this bull market still has a way to go and expect the technology sector to lead. LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains an overweight stance on the technology sector, as well as industrials, both positioned to benefit from the buildout and adoption of AI.